BRUSSELS (AFP) ― The eurozone is in

“critical” danger but can restore credibility with speedy moves towards a

banking union, some form of pooled debt and if the European Central Bank pumps

in more cash, the IMF said on Wednesday.

The European Central Bank should use more of its special measures to buy government debt and fund banks, the IMF said, all steps that EU paymaster Germany sees as major initiatives only possible in return for a much tighter political and fiscal union.

In a hard-hitting review of policies for the euro area, the IMF warned: “The euro area crisis has reached a new and critical stage.

“Despite major policy actions, financial markets in parts of the region remain under acute stress, raising questions about the viability of the monetary union itself.”

A worsening of the crisis would have a big impact on neighboring European countries “and the rest of the world.”

It warned: “A determined move toward a more complete union is needed now.”

On growth, the International Monetary Fund said the “stark” truth was that eurozone countries had lagged the best performers for 50 years.

The euro is slightly over-valued by zero to 5.0 percent, the IMF estimated, but some countries in crisis needed a much bigger adjustment, of 5.0-10 percent for Italy and 10-15 percent for Spain.

Determined programs for structural reforms to raise competitiveness were vital, the IMF said, warning also of a risk of deflation and suggesting that strong countries in northern Europe could allow wages and inflation to rise.

German Chancellor Angela Merkel on Wednesday defended Germany’s attitude towards getting out of the crisis, adding that though she was optimistic, she could not be certain that the “European project” would work.

Merkel stressed that Germans largely shared the “fundamental principles,” namely “no solidarity without corresponding effort and no guarantees without control.”

The view of the IMF is particularly significant because the fund is committed with the EU to direct bailouts for Greece, Ireland and Portugal, in defining the conditions and auditing the progress of rescue programs.

The IMF stressed that the key to growth was further action to put over-strained public finances on a sound basis, coupled with longer-term reforms to increase efficiency.

“The first priority is a banking union for the euro area,” the IMF said, which could combine a pan-European scheme to guarantee bank deposits and common bank supervision.

The IMF said “welcome” progress was made in this direction at an EU summit in late June but that reform efforts must be urgently sped up.

Moreover, any banking union had to be backed by fiscal integration and “more risk sharing” to prevent a shock in one country from imperilling the entire eurozone, the IMF said.

The “introduction of a limited form of common debt” could be a half-way step towards “fiscal integration and risk sharing,” it said in reference to some form of common bonds for the eurozone.

The IMF also argued that the ECB still had room to reduce interest rates, could announce a big program to buy bonds on the secondary market and mount more operations guaranteeing banks access to cheap funds for several years.

The fund urged EU authorities to make clear that the ECB and the rescue funds would not have priority over private investors in the event of a default.

“A clear commitment to accept equal status ... as in the case of Spain” would boost confidence, the IMF said, referring to a rescue for Spanish banks.

The IMF added that “long-standing structural rigidities need to be tackled to raise long-term growth prospects”, focusing on “improving competitiveness.” This was “essential”, it said.

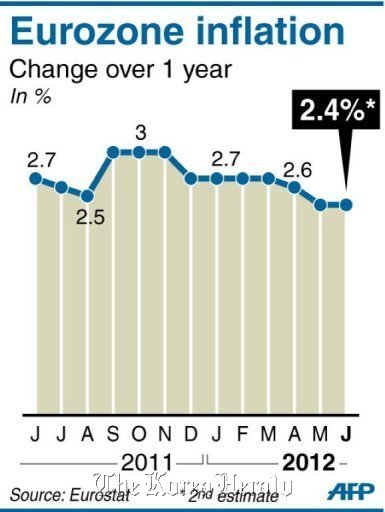

It added that the economic outlook was bleak, with average eurozone growth of 1.5 percent in 2011, giving way to contraction of 0.3 percent this year and a return to growth at 0.7 percent next year.

Unemployment rates would remain high this year, from 5.5 percent in Germany to 24 percent in Spain, and these differences would persist.

The risk of deflation was low in the faster-growing economies but “significant in the periphery.”

Currencies Direct senior analyst Alistair Cotton said the IMF warning on deflation “has set alarm bells ringing around the eurozone.

“The euro is already under tremendous pressure, and deflation will cause a huge problem for countries like Italy, with high levels of outstanding debt because it raises the real value of that debt,” he said.

The ECB, Cotton added “needs to adapt to changing circumstances” otherwise it faces the “real prospect of being the most conventional of central banks of a failed currency area.”

The European Central Bank should use more of its special measures to buy government debt and fund banks, the IMF said, all steps that EU paymaster Germany sees as major initiatives only possible in return for a much tighter political and fiscal union.

In a hard-hitting review of policies for the euro area, the IMF warned: “The euro area crisis has reached a new and critical stage.

“Despite major policy actions, financial markets in parts of the region remain under acute stress, raising questions about the viability of the monetary union itself.”

|

| One euro and one pound coins sit on euro notes in this arranged photograph in London. (Bloomberg) |

A worsening of the crisis would have a big impact on neighboring European countries “and the rest of the world.”

It warned: “A determined move toward a more complete union is needed now.”

On growth, the International Monetary Fund said the “stark” truth was that eurozone countries had lagged the best performers for 50 years.

The euro is slightly over-valued by zero to 5.0 percent, the IMF estimated, but some countries in crisis needed a much bigger adjustment, of 5.0-10 percent for Italy and 10-15 percent for Spain.

Determined programs for structural reforms to raise competitiveness were vital, the IMF said, warning also of a risk of deflation and suggesting that strong countries in northern Europe could allow wages and inflation to rise.

German Chancellor Angela Merkel on Wednesday defended Germany’s attitude towards getting out of the crisis, adding that though she was optimistic, she could not be certain that the “European project” would work.

Merkel stressed that Germans largely shared the “fundamental principles,” namely “no solidarity without corresponding effort and no guarantees without control.”

The view of the IMF is particularly significant because the fund is committed with the EU to direct bailouts for Greece, Ireland and Portugal, in defining the conditions and auditing the progress of rescue programs.

The IMF stressed that the key to growth was further action to put over-strained public finances on a sound basis, coupled with longer-term reforms to increase efficiency.

“The first priority is a banking union for the euro area,” the IMF said, which could combine a pan-European scheme to guarantee bank deposits and common bank supervision.

The IMF said “welcome” progress was made in this direction at an EU summit in late June but that reform efforts must be urgently sped up.

Moreover, any banking union had to be backed by fiscal integration and “more risk sharing” to prevent a shock in one country from imperilling the entire eurozone, the IMF said.

The “introduction of a limited form of common debt” could be a half-way step towards “fiscal integration and risk sharing,” it said in reference to some form of common bonds for the eurozone.

The IMF also argued that the ECB still had room to reduce interest rates, could announce a big program to buy bonds on the secondary market and mount more operations guaranteeing banks access to cheap funds for several years.

The fund urged EU authorities to make clear that the ECB and the rescue funds would not have priority over private investors in the event of a default.

“A clear commitment to accept equal status ... as in the case of Spain” would boost confidence, the IMF said, referring to a rescue for Spanish banks.

The IMF added that “long-standing structural rigidities need to be tackled to raise long-term growth prospects”, focusing on “improving competitiveness.” This was “essential”, it said.

It added that the economic outlook was bleak, with average eurozone growth of 1.5 percent in 2011, giving way to contraction of 0.3 percent this year and a return to growth at 0.7 percent next year.

Unemployment rates would remain high this year, from 5.5 percent in Germany to 24 percent in Spain, and these differences would persist.

The risk of deflation was low in the faster-growing economies but “significant in the periphery.”

Currencies Direct senior analyst Alistair Cotton said the IMF warning on deflation “has set alarm bells ringing around the eurozone.

“The euro is already under tremendous pressure, and deflation will cause a huge problem for countries like Italy, with high levels of outstanding debt because it raises the real value of that debt,” he said.

The ECB, Cotton added “needs to adapt to changing circumstances” otherwise it faces the “real prospect of being the most conventional of central banks of a failed currency area.”

.jpg)